Mūsų komandos naujausi publikuoti moksliniai tyrimai

2018

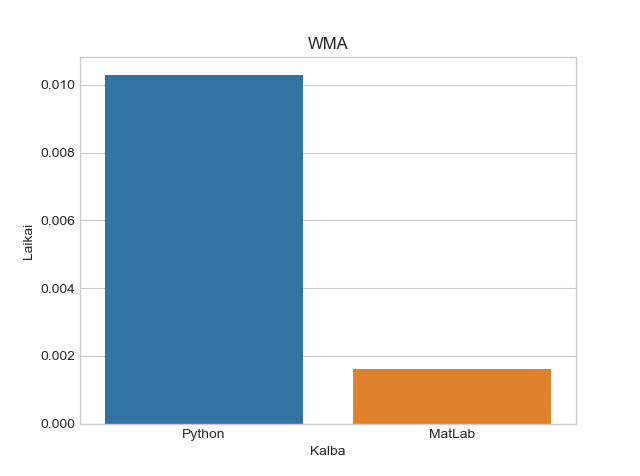

„Python and MATLAB performance comparison in algorithmic trading.“

In this research several algorithmic trading strategies are tested on both Python and MATLAB programming languages in order to show the performance differences in terms of execution time. In the first section of the research basic vectorised operations are compared with the equivalent operations using for loops to show the overall Python and MATLAB speed performance. In the later sections specific algorithmic trading strategies’ implementation scripts are executed to show how both languages cope with importing, tidying and wrangling data as well as with basic optimization. From the generated results in the majority of tasks MATLAB significantly outperformed Python. Therefore, our team uses MATLAB as a main programming and computing software.

2017

„Atomic Order Execution Tactics in Futures Markets: a Simulation

Study Using Real World Market Data.“

This research investigates a better way to execute buy or sell orders in the futures markets than using instant market orders. The goal of this research is to optimize orders execution to make it cheaper. For most futures our proposed methods have given significantly better order execution costs than executing with widely used execution method (market orders).

2016

„Portfolio of Global Futures Algorithmic Trading Strategies for Best Out-of-Sample Performance.“

We investigate two different portfolio construction methods for two different sets of algorithmic trading strategies that trade global futures. The problem becomes complex if we consider the out-of-sample performance.

„Pareto Optimised Moving Average Smoothing For Futures and Stock Trend Predictions.“

We propose a Pareto optimised moving average method where the essence is weight optimisation, so that for every level of smoothness we obtain the best accuracy. The new method outperforms other popular moving average methods in the majority of cases. Traders can use this method to detect trends earlier and to avoid unnecessary trading and increase the profitability of their strategies.

„Analysis of Execution Methods in US and European Futures.“

Order execution methods using various combinations of limit and market orders in U.S. and European futures markets are investigated in this research. It is concluded that transaction costs can be reduced up to 70% for some markets in comparison to instant market order method.

2014

„Multi-agent system based on oscillating agents for portfolio design.“

Improved cellular-automaton-based models of excitable media were employed to mimic economic and financial units in rapidly changing environments. It was shown that the use of fast Fourier transformation and selection of moderate number of spectra principal components is an important source of inexplicit additional information about processes in the financial markets. We demonstrated that the presence of random fluctuations, oscillations that one observes in wave propagation patters can be classified by employing the spectral features.

„Novel Automated Multi-agent Investment System Based on Simulation of Self-excitatory Oscillations.“

In this paper we investigate how to (i) mode/ spread of self-excited oscillations in social mediums and (ii) simulate data series of rare events’ (e.g. crises). We proposed a novel multi-agent investment simulation system, composed from a multitude of artificial investing agents. Consequently, we developed a simulation tool, which can deal with self-excited oscillations and high dimensionality small sample size problems arising in the modern financial markets.

„Optimal negative weight moving average for stock price series smoothing.“

We propose an optimal weighting scheme for smoothing stock price data. For a given smoothness level we minimise fitting error. We discovered that negative weights have quite a small influence on the overall performance of moving averages.

„Sustainable economy inspired large-scale feed-forward portfolio construction.“

To understand large-scale portfolio construction tasks we analyse sustainable economy problems by splitting up large tasks into smaller ones and offer an evolutional feed-forward system-based approach. The theoretical justification for our solution is based on multivariate statistical analysis of multidimensional investment tasks, particularly on relations between data size, algorithm complexity and portfolio efficacy.

2013

„Intraday forex bid/ask spread patterns-Analysis and forecasting.“

We searched for liquidity patterns during 24h trading sessions. After experimental comparison, we found that neural networks and regression trees are most suitable for liquidity forecasting and outperform simple averaging and regression. We also rated the factors that most influence forecasting accuracy. We conclude that in most currency pairs the liquidity can be forecasted more accurately than the simple averaging which is often used in practice for planning large order execution.

„How (in) efficient is after-hours trading?“

In this research we analyze US stock market after-hours trading. During this time the market is thinly traded and the possibility of price (in)efficiency arises. We create a portfolio of ~400 automated trading strategies which try to exploit inefficiencies. The average portfolio performance is a 23 percent per annum with a Sharpe ratio of 4. This shows that prices are inefficient during after-hours trading in the US stock market.

2012

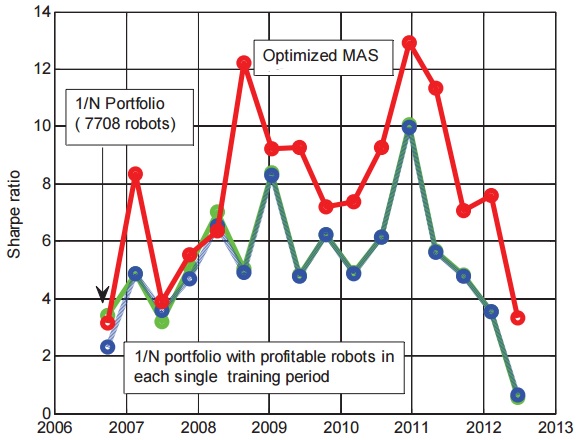

„Multi-agent system based portfolio management in prior-to-crisis and crisis period.“

We analyze portfolio creation techniques in a high frequency trading domain and randomly changing environments. We aim to create the best risk/reward portfolio based on thousands

of profit histories of automated trading robots. Experiments with 7708-dimensional 2004-2012 data confirm the effectiveness of our new approach.

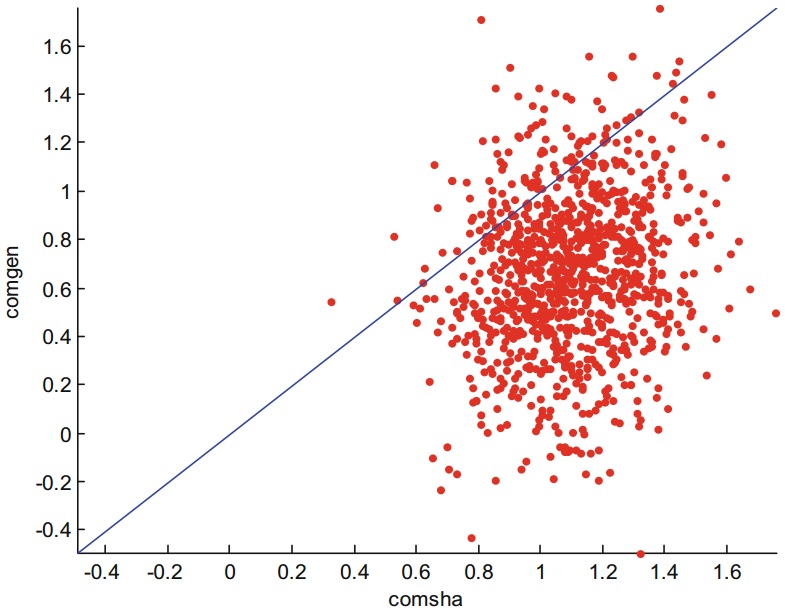

„Discrete portfolio optimisation for large scale systematic trading applications.“

Markowitz’s mean-variance portfolio optimisation is not suitable for a large number of assets due to the unacceptably slow quadratic optimisation procedure involved. We propose a much faster heuristic approach that scales linearly rather than the quadratic scaling in the Markowitz method. Moreover, our proposed approach, Comgen, is on average better than the Markowitz approach when applied to unseen data.

„Synthetic History for Exchange Traded Funds.“

To make money in trading one ought to forecast the future price, but to do so accurately one must verify the predictions using the past data. A short trading history can present a problem. We showed both theoretically and experimentally that the history of some financial assets can be reconstructed quite accurately. We forecasted the past price movements of exchange traded funds (ETFs). The problem in practice is very acute as there are a number of very liquid ETFs that can be traded with minimum slippage but their available history is too short. In such situations systematic traders cannot test their trading models as the history length is insufficient.

„Three decision making levels in portfolio management.“

To improve portfolio management process we suggest using history of automated trading strategies instead of actual assets. We developed the three level decision making systems aimed to find the portfolio weights.